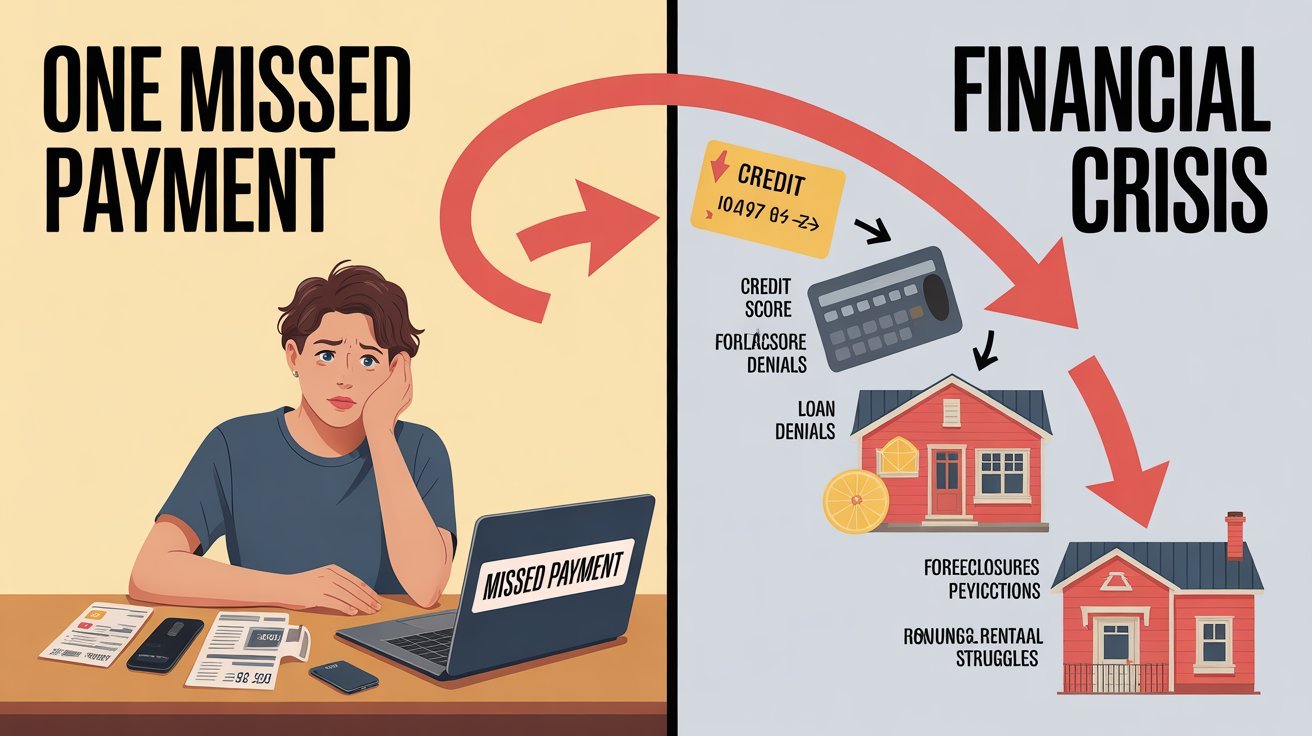

Falling behind on student loan payments can feel like a small issue at first—but it can quickly turn into a serious financial problem. One missed payment might not seem like a big deal, but over time, delinquent student loans can trigger a sharp credit score plunge that affects your entire financial life.

In 2026, with rising living costs and financial pressure on borrowers, more people are struggling to keep up with loan payments. The consequences go far beyond late fees. A damaged credit score can impact your ability to get approved for credit cards, mortgages, car loans, or even rental housing.

Many borrowers don’t fully understand how quickly delinquency affects their credit. Within just 30 days of a missed payment, lenders may report it to credit bureaus, causing immediate score drops.

A common mistake I’ve seen is assuming you can “catch up later” without consequences. In reality, the longer a loan remains delinquent, the more severe the financial damage becomes.

In this guide, you’ll learn exactly how delinquent student loans impact your credit score, how much your score can drop, and—most importantly—how to recover and rebuild your financial stability.

What Are Delinquent Student Loans?

Delinquent student loans are loans that have missed one or more scheduled payments. A loan becomes delinquent the day after a payment is missed.

Key Terms Explained

| Term | Meaning | Real Example |

|---|---|---|

| Delinquency | Missed payment | 30 days late |

| Default | Severe delinquency (270+ days) | Loan sent to collections |

| Credit report | Financial history record | Used by lenders |

| Credit score | Risk rating (300–850) | Affects loan approval |

Real-World Example

If a borrower misses a $300 monthly payment, the loan becomes delinquent immediately. After 30 days, it may be reported to credit bureaus, causing a noticeable drop in credit score.

Why This Matters

Delinquency is the first stage of financial trouble. If not addressed quickly, it can escalate into default, which has much more serious consequences.

In most real-world cases, early-stage delinquency is the easiest point to fix—but also the most ignored.

Why Delinquent Student Loans Cause Credit Score Plunge

Credit scores are heavily influenced by payment history, which makes up about 35% of your total score. This means missed payments have a direct and immediate impact.

Impact Table

| Factor | Impact Level | Effect |

|---|---|---|

| Missed payments | Very High | Immediate score drop |

| Loan default | Extreme | Severe damage |

| Collections | Extreme | Long-term negative mark |

| Payment history | Critical | 35% of score |

When a student loan becomes delinquent, lenders report the missed payment to credit bureaus. This negative mark lowers your score and remains on your credit report for years.

Example Impact

- 30 days late → -50 to -80 points

- 90 days late → -100+ points

- Default → Major long-term damage

In most real-world cases, the first 60–90 days of delinquency cause the fastest and most severe credit score decline.

Latest Student Loan Delinquency Trends (2024–2026)

Student loan delinquency has become a growing financial concern in recent years. Economic pressure, inflation, and the end of relief programs have made it harder for many borrowers to stay current on payments.

Student Loan Trends

| Year | Data | What It Means |

|---|---|---|

| 2024 | Repayment programs resumed | Borrowers under pressure |

| 2025 | Increase in missed payments | Rising delinquency rates |

| 2026 | Higher defaults expected | Credit risk growing |

One major shift occurred when temporary payment relief programs ended, forcing millions of borrowers back into repayment. Many were unprepared for the sudden return of monthly obligations.

Another trend is the increasing number of borrowers entering early-stage delinquency (30–90 days late). This stage is critical because it’s where credit scores begin to drop significantly.

Lenders and credit agencies are now more focused on real-time reporting, meaning missed payments are reflected faster than in previous years.

Why These Trends Matter

These trends show that more people are experiencing credit score drops due to student loans. Understanding this helps you act early and avoid long-term damage.

In most real-world cases, borrowers who act within the first 30 days of delinquency avoid the worst credit damage.

How Credit Scores Are Calculated

To fully understand why delinquent student loans cause a credit score plunge, you need to know how credit scores work.

Credit scores are calculated using multiple factors, but not all factors have the same impact.

Credit Score Breakdown

| Factor | Weight | Impact |

|---|---|---|

| Payment history | 35% | Most important |

| Credit utilization | 30% | High impact |

| Credit history length | 15% | Medium |

| Credit mix | 10% | Low |

| New credit inquiries | 10% | Low |

Payment History (The Biggest Factor)

Payment history is the most critical part of your credit score. When you miss a student loan payment, it directly affects this category, causing an immediate drop.

Credit Utilization

Although more relevant for credit cards, utilization still plays a role in overall credit health. High balances can worsen the impact of delinquency.

Length of Credit History

Older accounts help stabilize your score, but they cannot fully offset missed payments.

Credit Mix & Inquiries

These factors have smaller effects but still contribute to your overall score.

Key Insight

Even one missed payment can outweigh years of good credit behavior.

A common mistake I’ve seen is focusing on credit utilization while ignoring payment history—which is far more important.

How Much Your Credit Score Can Drop

One of the biggest concerns borrowers have is how severely delinquent student loans can impact their credit score. The reality is that the drop can be significant—and it often happens faster than expected.

The exact impact depends on your starting score, payment history, and how long the loan remains delinquent.

Credit Score Drop Scenarios

| Situation | Starting Score | Estimated Drop | New Score |

|---|---|---|---|

| 30 days late | 720 | -60 points | 660 |

| 60 days late | 700 | -80 points | 620 |

| 90 days late | 680 | -100 to -120 | 560–580 |

| Default (270+ days) | 700 | -150+ points | 550 or lower |

Borrowers with higher credit scores often experience larger drops because they have more to lose. A person with excellent credit (750+) may see a sharper decline than someone with already low credit.

Real-World Scenario

A borrower with a 720 score misses two payments and becomes 60 days delinquent. Their score drops to around 620, pushing them from “good credit” to “fair credit.” This change can lead to:

- Higher interest rates

- Loan rejections

- Reduced credit limits

Key Insight

The first 90 days of delinquency cause the most damage. After that, the impact continues but at a slower pace.

In most real-world cases, recovering from a 100-point drop takes months to years, not weeks.

Delinquency vs Default

Many borrowers confuse delinquency with default, but they are very different stages—and the consequences escalate dramatically.

Comparison Table

| Stage | Timeframe | Consequences | Severity |

|---|---|---|---|

| Delinquency | 1–269 days late | Credit score damage | High |

| Default | 270+ days late | Collections, legal action | Extreme |

Delinquency (Early Stage)

Delinquency begins immediately after a missed payment. At this stage:

- You can still catch up

- Credit damage is reversible

- Lenders may offer assistance

This is the best time to act.

Default (Severe Stage)

Federal student loans typically enter default after 270 days (about 9 months) of missed payments.

At this stage:

- The loan may be sent to collections

- Wage garnishment can occur

- Tax refunds may be withheld

- Credit damage becomes long-term

Long-Term Impact of Default

Default can remain on your credit report for up to 7 years, making it much harder to access credit or secure favorable financial terms.

Key Insight

Delinquency is a warning sign. Default is a financial crisis.

A common mistake I’ve seen is ignoring delinquency notices—by the time borrowers react, the loan is already close to default.

Step-by-Step Plan to Fix Delinquent Student Loans

If your student loans are already delinquent, the most important thing is to act quickly. The longer you wait, the more severe the credit score plunge becomes. The good news is that early action can significantly reduce long-term damage.

The first step is to confirm your loan status. Check whether your loan is 30, 60, or 90+ days late. This determines how urgent your situation is and what options are still available.

The second step is contacting your loan servicer immediately. Many borrowers avoid this step, but lenders often provide solutions such as temporary payment plans or hardship assistance. Ignoring communication only accelerates the problem.

The third step is making at least a partial payment if possible. Even a partial payment can sometimes prevent further escalation or demonstrate good faith, depending on the lender’s policies.

The fourth step is choosing the right repayment strategy. Options such as income-driven repayment plans can reduce your monthly payments and make them more manageable.

Finally, set up automatic payments to avoid missing future due dates. Preventing additional missed payments is critical to stabilizing your credit score.

Micro-Expert Insight

In most real-world cases, borrowers who take action within the first 60 days avoid long-term credit damage.

How to Stop Credit Score Damage Fast

Stopping the credit score decline should be your top priority once delinquency begins. The goal is to prevent further negative reporting and stabilize your financial profile.

The fastest way to stop damage is to bring the account current. Once payments are up to date, no new negative marks are added to your credit report.

Another effective strategy is negotiating with your loan servicer. In some cases, lenders may offer short-term relief programs that prevent further reporting of missed payments.

You can also request deferment or forbearance if you are experiencing financial hardship. These options temporarily pause or reduce payments, helping you avoid deeper delinquency.

Monitoring your credit report is also important. This ensures that all reported information is accurate and allows you to detect any errors that may worsen your score.

Damage Control Strategies

| Strategy | Speed | Effectiveness |

|---|---|---|

| Bring account current | Fast | Very High |

| Contact lender | Fast | High |

| Deferment/forbearance | Medium | High |

| Credit monitoring | Medium | Medium |

Key Insight

Stopping further damage is more important than fixing past damage in the early stages.

Micro-Expert Insight

A common mistake I’ve seen is focusing on repairing credit before stopping ongoing delinquency.

Repayment Options

If you cannot afford your current payments, several programs can help you manage delinquent student loans more effectively.

Income-Driven Repayment Plans

These plans adjust your monthly payment based on your income and family size. In many cases, payments can be reduced significantly, making it easier to stay current.

Deferment

Deferment allows you to temporarily pause payments under specific conditions, such as unemployment or financial hardship. Interest may or may not continue to accrue depending on the loan type.

Forbearance

Forbearance also pauses or reduces payments, but interest usually continues to accumulate. It is typically used as a short-term solution.

Loan Rehabilitation

Loan rehabilitation is one of the most powerful tools for borrowers in default. It involves making a series of agreed-upon payments to bring the loan back into good standing.

Repayment Options Comparison

| Option | Best For | Impact on Credit |

|---|---|---|

| Income-driven plan | Long-term affordability | Positive |

| Deferment | Temporary hardship | Neutral |

| Forbearance | Short-term relief | Neutral–Negative |

| Rehabilitation | Default recovery | Positive (long-term) |

Key Insight

Choosing the right repayment option depends on your financial situation and how far delinquency has progressed.

In most real-world cases, income-driven repayment plans are the most sustainable long-term solution for borrowers.

Common Mistakes That Worsen Credit Score Damage

When dealing with delinquent student loans, certain mistakes can make the situation significantly worse. Many borrowers unintentionally accelerate their credit score plunge simply by delaying action or misunderstanding how the system works.

One of the biggest mistakes is ignoring the problem. Some borrowers avoid opening emails or answering calls from loan servicers, hoping the issue will resolve itself. In reality, missed payments continue to be reported, making the damage worse each month.

Another common mistake is making inconsistent payments. Paying sporadically without a structured plan can keep the loan in delinquent status, meaning your credit score continues to suffer despite partial efforts.

Some borrowers also prioritize other debts over student loans without considering the impact on their credit profile. While balancing obligations is important, student loan delinquency carries long-term consequences that should not be overlooked.

Additionally, many people fail to explore available repayment options such as income-driven plans or deferment. These programs exist specifically to prevent delinquency from escalating.

Micro-Expert Insight

In most real-world cases, delay—not inability to pay—is the main reason delinquency turns into default.

Hidden Consequences of Student Loan Default

Defaulting on student loans goes far beyond a credit score drop. It introduces serious financial and legal consequences that can affect multiple areas of your life.

One of the most severe consequences is wage garnishment, where a portion of your paycheck is automatically deducted to repay the loan. This can happen without a court order for federal student loans.

Another major consequence is the loss of tax refunds. Government agencies can intercept your tax refund and apply it toward your loan balance.

Default can also lead to collections activity, where third-party agencies attempt to recover the debt. This often adds additional fees and further damages your credit.

In some cases, borrowers may also lose access to additional financial aid, making it harder to return to school or pursue further education.

Default Consequences Breakdown

| Consequence | Impact Level | Long-Term Effect |

|---|---|---|

| Wage garnishment | Very High | Reduced income |

| Tax refund seizure | High | Loss of funds |

| Collections fees | High | Increased debt |

| Credit damage | Extreme | 7+ years impact |

Key Insight

Default is not just a credit issue—it becomes a legal and financial burden.

A common mistake I’ve seen is underestimating how aggressive collections can become after default.

Tools & Resources to Rebuild Credit Faster

Once the damage has occurred, rebuilding your credit becomes the next priority. While recovery takes time, the right tools and strategies can accelerate the process.

One of the most effective tools is consistent on-time payments. Even after delinquency, establishing a new positive payment history gradually improves your credit score.

Credit monitoring services can help track your progress and alert you to changes or errors on your report. This ensures that all information is accurate and up to date.

Secured credit cards are another useful tool. They allow borrowers to rebuild credit by demonstrating responsible usage and consistent payments.

Debt management plans and financial counseling services can also provide structured guidance, especially for borrowers dealing with multiple debts.

Credit Rebuilding Tools

| Tool | Purpose | Effectiveness |

|---|---|---|

| On-time payments | Build positive history | Very High |

| Credit monitoring | Track progress | Medium |

| Secured credit cards | Rebuild credit | High |

| Financial counseling | Strategy guidance | Medium–High |

Key Insight

Credit recovery is a long-term process, but consistent positive behavior leads to steady improvement.

In most real-world cases, borrowers begin to see noticeable credit improvement within 3–6 months of consistent on-time payments.

FAQ

1. How fast do student loans affect my credit score after a missed payment?

A missed student loan payment can affect your credit within 30 days. Once reported to credit bureaus, it can trigger a noticeable score drop, especially if you previously had good credit.

2. How much can delinquent student loans lower my credit score?

The drop varies, but typical ranges include:

- 30 days late: -50 to -80 points

- 60–90 days late: -80 to -120 points

- Default: -150 points or more

The higher your starting score, the more dramatic the drop can feel.

3. What is the difference between delinquency and default?

Delinquency begins immediately after a missed payment. Default happens after about 270 days of non-payment for federal student loans. Default has more severe consequences, including collections and wage garnishment.

4. Can I recover my credit after student loan delinquency?

Yes. Credit recovery is possible through consistent on-time payments, enrolling in repayment plans, and reducing other debt. Many borrowers begin seeing improvement within 3–6 months of corrective action.

5. Will paying off delinquent student loans remove the damage?

Paying off the loan stops further damage, but past late payments may still remain on your credit report for up to 7 years. However, their impact decreases over time.

6. What is the fastest way to stop credit score damage?

The fastest way is to bring the account current and contact your loan servicer immediately. This prevents additional negative reporting and stabilizes your credit profile.

In most real-world cases, stopping further delinquency matters more than trying to quickly “fix” past damage.

Related Topics

You may also like:

Conclusion — How to Recover From a Credit Score Plunge

Delinquent student loans can cause a serious credit score plunge, but the situation is not permanent. The key is understanding how quickly damage occurs and taking action before it escalates into default.

Throughout this guide, we explored how missed student loan payments impact credit scores, why even one late payment matters, and how borrowers can experience drops of 50 to 150+ points depending on severity. We also covered the difference between delinquency and default, along with recovery strategies that can help rebuild financial stability.

The most important takeaway is that early action changes everything. The sooner you contact your loan servicer, explore repayment options, and bring your account current, the better your long-term credit outcome will be.

Final Action Step

If your student loans are delinquent, take immediate action:

- Contact your loan servicer

- Explore income-driven repayment options

- Bring your account current as soon as possible

- Monitor your credit report regularly

In most real-world cases, borrowers who act within the first 30–60 days of delinquency avoid the most severe long-term credit damage and recover significantly faster than those who delay action.